Hijacking CashAppFriday

Facts:

Peer-to-peer (P2P) payment apps — like CashApp, Zelle, and Venmo — make it easy for users to send money to friends and family instantly, in just a few clicks.

All they have to do is download one of these apps, create an account, and add a bank account or credit card.

Users can then send and receive money from other users, and deposit these funds into a bank account of their choosing.

But unlike money in the bank, account balances stored in these P2P apps do not have the same consumer protections as a credit or debit card.

In other words, once the money has been sent, it’s gone for good. And scammers are using this loophole to take advantage of unsuspecting consumers.

A Cautionary Tale

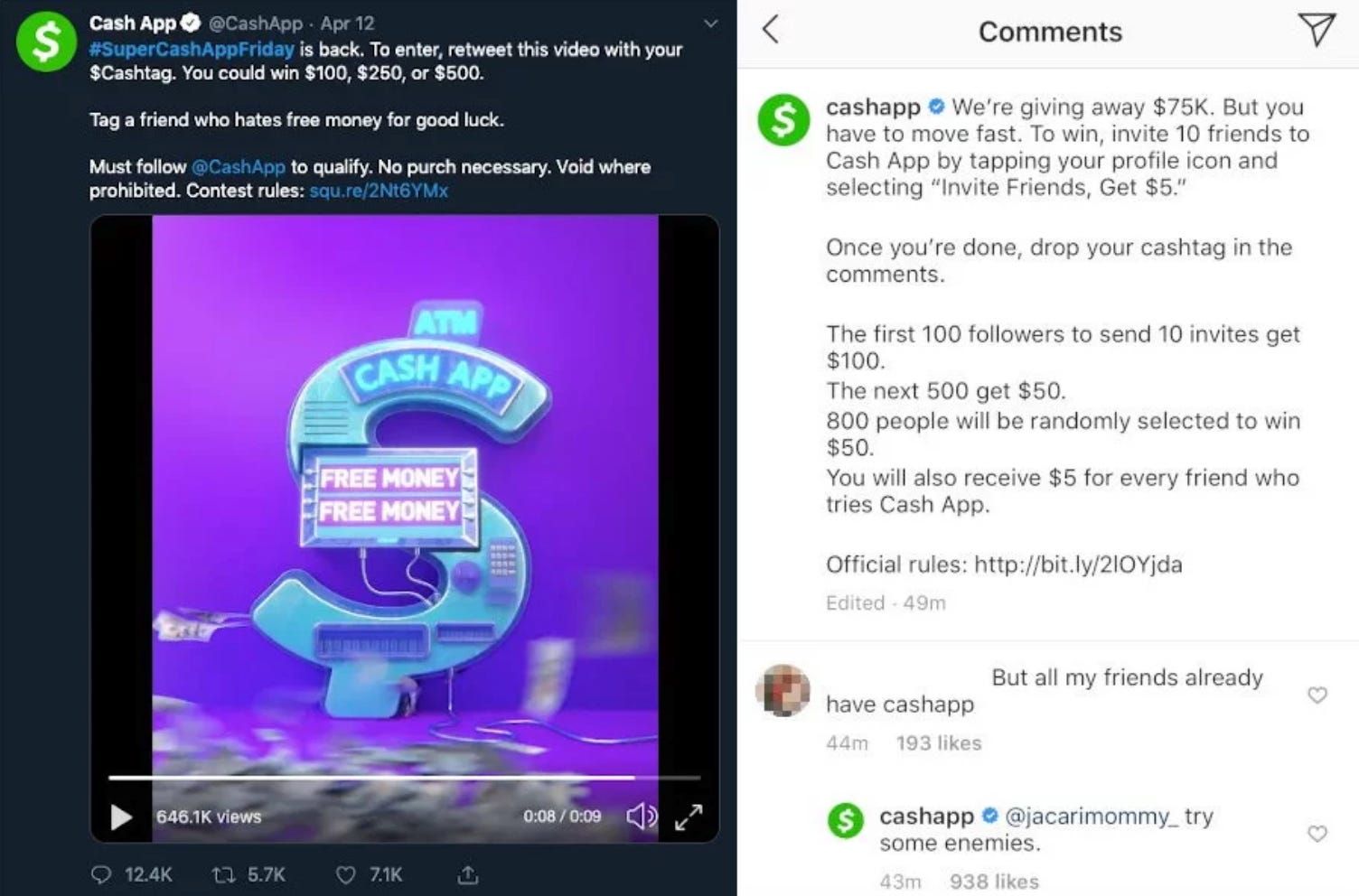

Back in 2017, Cash App came up with a brilliant marketing ploy to promote their P2P payment service: begin running a weekly giveaway on social media, using the hashtag #CashAppFriday.

The plan was simple: Cash App would post about the giveaway every Friday, using the hashtag on Instagram and Twitter. Users could then enter to win by inviting friends, retweeting, or replying to these posts with their $cashtag — a unique ID used for sending and receiving money. From there, the company would randomly select winners and deposit an unspecified amount of money into their Cash App accounts.

Their plan worked.

The campaign has become a huge hit among social media users, resulting in a continuous stream of downloads and sign-ups. In fact, the app has been downloaded over 59.8 million times since then, and #CashAppFriday is still going strong.

Source: Tenable

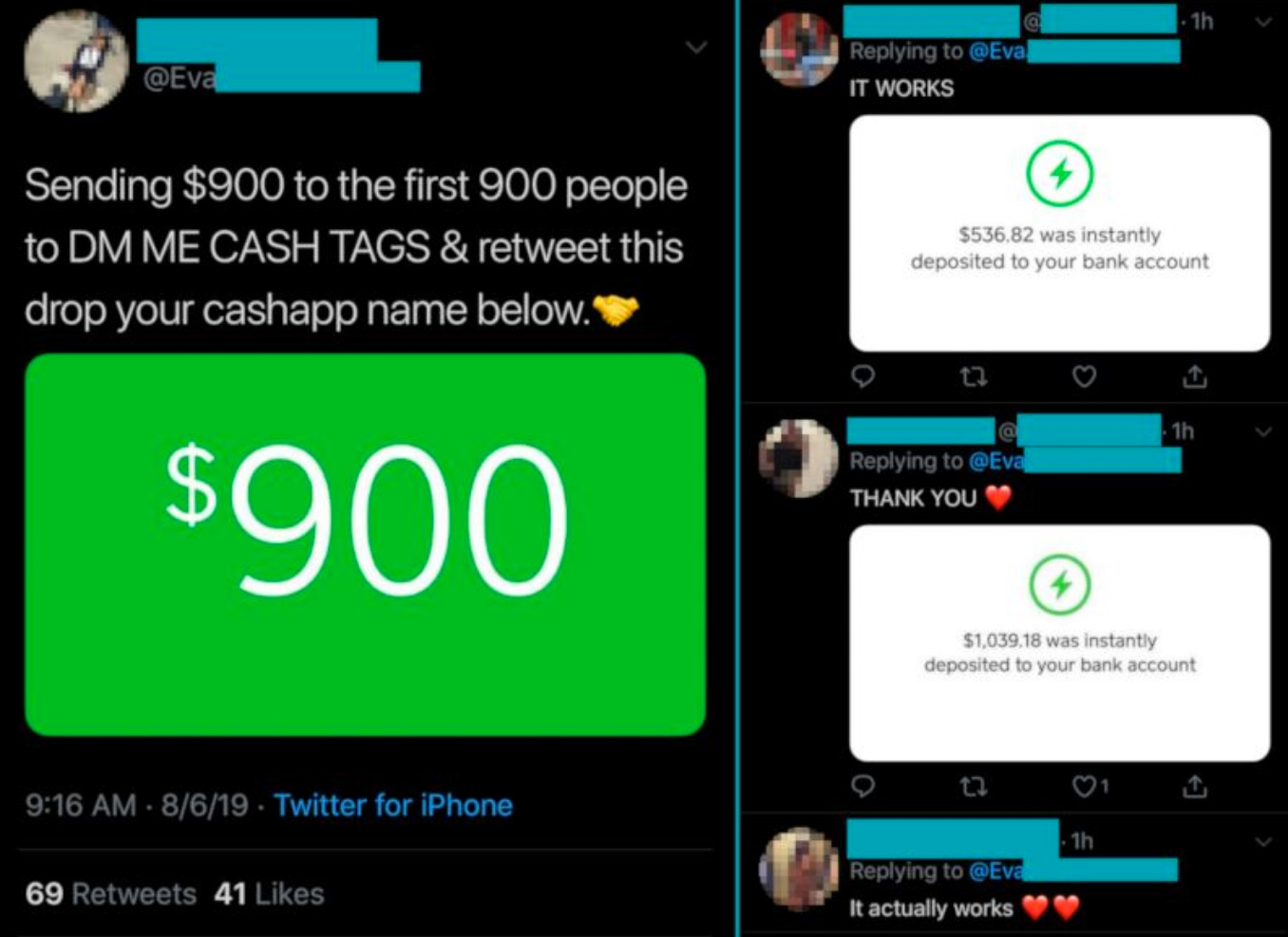

Of course, the success of these campaigns also made con artists sit up and take notice. And it wasn’t long before they decided to start their own game. Using the same hashtag from the real Cash App giveaways, they began employing a variety of tactics to separate social media users from their hard-earned cash. Among the most popular of these was promising huge amounts of money in exchange for a small fee.

Just like that, the #CashAppFriday marketing ploy was twisted by scammers into a ripe supply of free money.

One of the victims was Jennifer Loran, a single mom who had been trying to win a #CashAppFriday giveaway for months. Then it happened: someone who claimed to work for Cash App reached out to tell her that she had been named one of the lucky winners. All she needed to do to claim her prize was pay a small verification deposit of $20.

Erring on the side of caution, Ms. Loran checked the employee’s social media profile. Sure enough, his profile picture was the Cash App logo and his display name said “Cash App”. During their exchange, Ms. Loran also got the impression that he knew a lot about the app. This put her at ease and she proceeded to send the $20 to the $cashtag he provided.

Within minutes of doing this, the man blocked her on all social media, ending their only means of communication. That’s when Ms. Loran realized she’d been scammed.

Frustrated by this turn of events, she reached out to Cash App to request a refund. Customer support replied by telling her that they could not cancel or refund the transaction, as the funds had already been withdrawn to the recipient’s bank account.

Sadly, Ms. Loran had no choice but to accept the loss and move on.

The Larger Scheme At Play

While P2P payment platforms, like Cash App, make it convenient to send money straight from your checking account, these transactions are often irreversible and don’t require much verification. In other words, it’s the ideal setup for scammers. In fact, thieves who once relied on stolen paper checks to drain your bank account are now switching over to P2P digital fraud as a lower-risk option.

Behind these so-called Cash App scam giveaways is a timeless con at work. The con is played out in Abbott and Costello’s Two Tens for a Five, in which an unsuspecting Costello is asked by Abbott if he can exchange two $10 bills for his $5 bill. This results in a $15 profit for Abbott and a $15 loss for Costello.

This con is known as money flipping or cash flipping. And most Cash App scam giveaways use this technique as their underlying foundation, with the occasional twist.

Money flippingv.: when one party claims they can take advantage of a system and turn a hundred dollars, for example, into a thousand.

The way this typically works is that a scammer will reach out to targets and claim that he can modify or “flip” P2P transactions, using a special software or because he has employee access to the payment platform. In order to “get in on the profits”, targets have to “front” a certain amount of money, ranging from as little as $10 all the way up to $1,000. In exchange for offering this service, the scammer asks for a small cut of the proceeds, which the victim can send him through Cash App.

Ms. Loran’s case was less obvious than this, but still operated on the same concept: send a $20 fee or “verification deposit”, receive $1000 in prize money.

Source: Tenable

If any of this sounds familiar, it’s probably because money flipping isn’t new — it just keeps reinventing itself. And while it’s been circulating around social media for years, what makes the Cash App version of money flipping so nefarious, and successful, is that it capitalizes on a legitimate giveaway promoted by a well-established, trusted company. Then it victimizes people who are hoping to win one of these coveted cash prizes.

It would appear that, as an unfortunate side effect of its success, Cash App’s marketing hashtag is attracting people who are in need of money and bad actors who exploit them. And all of this is happening in one place and without much regulation.

How It Works

This con is pretty simple and doesn’t take a whole lot of effort on the scammer’s part.

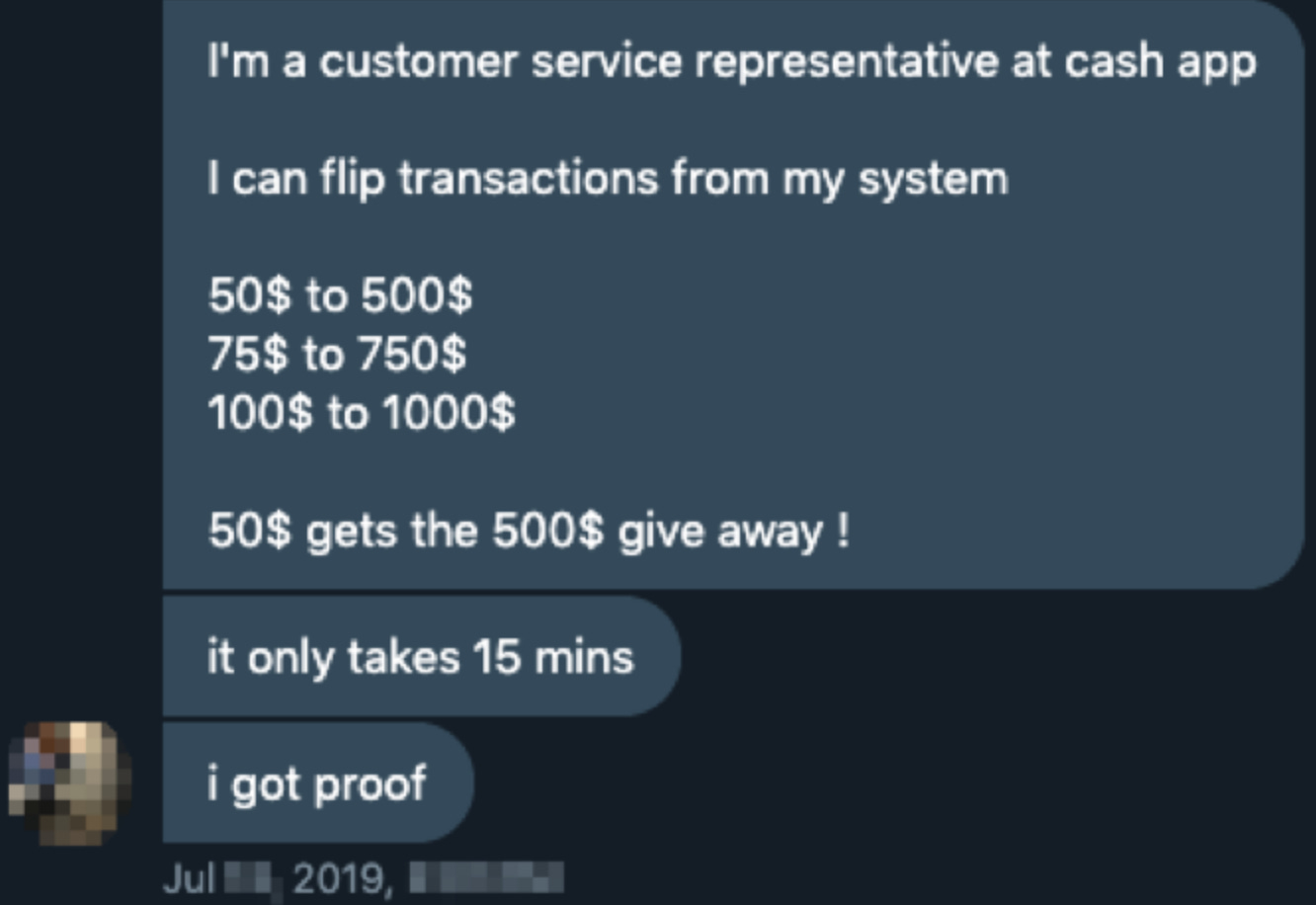

It starts with a direct message from a Cash App “customer service representative”. This individual will contact you out of nowhere and talk about how he has the ability to “flip transactions” within the Cash App system. He then lists various dollar amounts that might pique your interest. For example, if you front $50, he can turn it into $500. If you go in for $100, he does a little black magic on his end and shazam: $1000 for you! In other words, for a small fee and no effort on your part, you can laugh your way to the bank — in the span of only 15 minutes!

Oh, and he has proof.

Source: Tenable

However, if you start asking questions or pressing for more information, the scammer will stop responding.

But let’s say, for the sake of argument, you want to try your luck with this guy. So, you tell him you want in. Now what?

The “customer service rep” asks you to send an initial payment, verification deposit, processing fee — whatever you want to call it — to his $cashtag. So, you download Cash App from the App Store or open it up on your phone. From there, you enter the amount you want to send (let’s say $2.25), type in this guy’s $cashtag, state some ambiguous reason for sending the money, and tap the pay button.

Source: Online Tech Tips

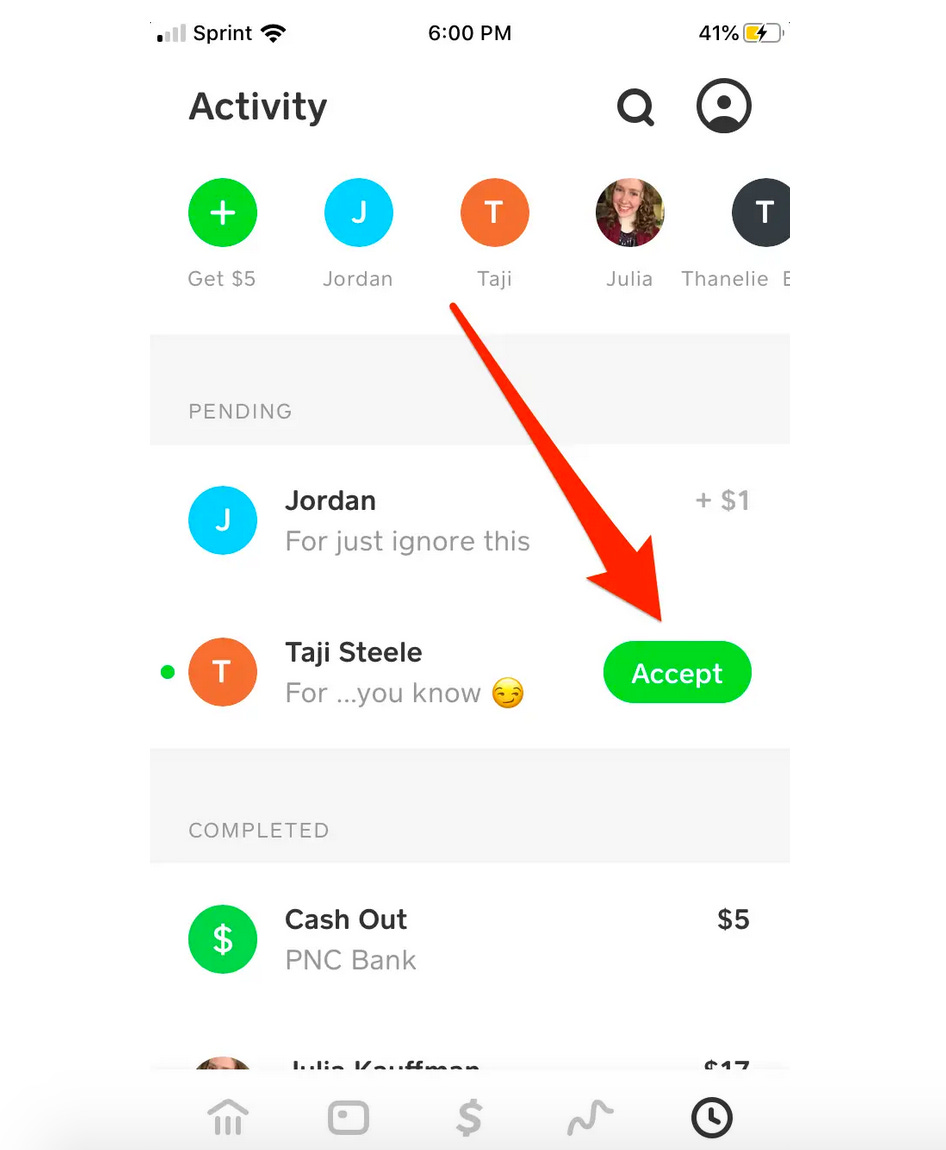

As soon as you initiate the transfer, the bank debits your account and the self-proclaimed “Cash App employee” receives this notification on his end:

Source: Business Insider

He quickly accepts your payment and withdraws it to his bank account, so that it can’t be reversed later on. Then he proceeds to cease all communication with you, which leaves you wondering what the hell just happened. But hey, at least part of what he promised came true: this whole process only took 15 minutes.

However, in some instances, you can “win” with these guys, even if it’s only temporary:

Some scammers may offer a smaller “flip” in order to gain your trust first. In other words, they may actually deliver on a promise to turn $2 into $20 to prove that the “flip” is real. This gets you excited enough to set your suspicions aside and go for round two. Only this time, you’ll buy in for $50 or $100 — and never hear from them again.

Take Steps to Protect Yourself

Situations like this are not exclusive to Cash App; they apply to any Peer-to-Peer payment platform. Therefore it’s important to proceed with caution and know what to watch out for. That said, follow these tips to get the most out of your P2P service with the least amount of risk:

Opt for stronger security. Almost all of the major P2P platforms offer the ability to create a personal identification number (PIN). Once that PIN is created, you’ll be required to type it in before each transfer. This extra layer of security protects your bank account from unauthorized withdrawals, in the event that your phone or account information fall into the wrong hands.

Only send money to people you know. Many peer-to-peer transactions are instantaneous and irreversible. Scammers know this and exploit it as much as they can. Therefore, it’s best to play it safe and only send funds to friends and family.

Get all of your recipient’s details correct from the get-go. Before you press “send” or “pay,” make sure that you have the right username, phone number, photo, or other identifier. Some services, such as Venmo, offer the opportunity to receive a special code to confirm that the person you’re sending money to is your intended recipient. Choose services that offer these features and use them.

Don’t use P2P services for business. Most P2P payment apps have terms that explicitly prohibit using them for commercial purposes, such as receiving payment for selling goods or services. In these instances, opt for a payment app such as Square Cash for Business or PayPal. This way, you’ll have an easier time getting your money back if the vendor doesn’t deliver.

Confirm that you can find help if things go wrong. Some P2P apps make users resolve their own disputes. Others offer significant help to resolve issues. Before using any P2P service, search through the app for customer service contact information and procedures so that you know where to go and what kind of help to expect.

Keep your app up-to-date. Hackers are always looking for vulnerabilities to exploit, while security professionals work around the clock to stop them. If you are using an outdated app, you’re probably missing the latest security patches and protections. Turn on auto-updates and this will be one less thing you have to worry about.

Final Notes and Updates

At the end of the day, digital payment services, like Cash App, were designed exclusively for sending money to family and friends — not for anything else. So, if you want to pay your part of the restaurant bill or send money to your nephew as a birthday gift, go right ahead. These platforms are easy to use and highly convenient.

However, if you choose to engage in any transactions beyond that, understand that you do so at your own risk. These companies will not protect you should you decide to send payment in exchange for undelivered products or too-good-to-be-true services. And that’s something that most users don’t realize when they first sign up. In fact, it’s easy to get a false sense of security from P2P apps, especially since so many banks promote them to their customers.

Despite this, peer-to-peer payment platforms are not managed by the bank; they are owned and operated by third-parties. Therefore, any transactions made over these networks are not insured, meaning that once the money is sent, it’s gone.

The reason you can’t ask for a refund or issue a chargeback is because, under the current law, P2P transactions are considered “authorized payments”, which voids your legal right to get your money back.

All of this to say, it’s best to think of P2P payments like cash: If you wouldn’t be comfortable giving this person a hundred-dollar bill, then don't use Cash App to send him $100. Once you do, that transaction is final and irreversible.

Useful Resources

To report a P2P scam:

https://secure.nclforms.org/nficweb/OnlineComplaintForm.aspx

The FTC’s tips for using P2P apps:

https://www.consumer.ftc.gov/blog/2018/02/tips-using-peer-peer-payment-systems-and-apps

Editor’s Note: Have you been affected by fraud? Most people have, in some form or another. If you have a story you would like to share, we’re sure our readers would benefit from hearing it. Please send an email to editor@theconartist.pub detailing your experience, and we will be in touch. Your privacy and any wishes of anonymity will be respected.

Thanks for reading! If you haven’t already, consider joining our community to receive in-depth exposés on the latest scams, hoaxes, and other forms of fraud.